Page 24 - CII Artha Magazine 2022

P. 24

Global Trends

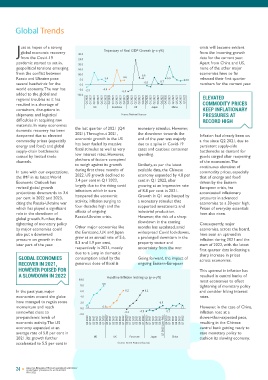

J ust as hopes of a strong Trajectory of Real GDP Growth (y-o-y%) crisis will become evident Impact on global 2.0 Key Policy Rates (%) 4.0 As per the UNCTAD’s

Global Trade Update, the

from the incoming growth

global economic recovery

from the Covid-19 30.0 data for the current year. growth due to the world trade in goods

25.0

pandemic started to set in, 20.0 Apart from China and US, 1.0 remained strong in 2021

geopolitical tensions emerging 15.0 none of the other major Russia-Ukraine crisis 3.5 and the export levels for

from the conflict between 10.0 6.6 economies have so far 0.0 all major economies rose

Russia and Ukraine pose 5.0 3.4 4.6 6.5 4.8 released their first quarter The Russian invasion of Ukraine above the pre-pandemic

several headwinds for the 0.0 -0.8 0.7 numbers for the current year. has rocked the global economy -1.0 3.0 level by the end of Q4.

world economy. The war has -5.0 -2.3 -4.4 -6.4 and nearly changed its economic Q1 2021 Q2 2021 Q3 2021 Q4 2021 Q1 2022 Q1 2021 Q2 2021 Q3 2021 Q4 2021 Q1 2022 Q1 2021 Q2 2021 Q3 2021 Q4 2021 Q1 2022 Q1 2021 Q2 2021 Q3 2021 Q4 2021 Q1 2022 Q1 2021 Q2 2021 Q3 2021 Q4 2021 Q1 2022 The positive trend for

added to the global and -10.0 outlook for the year. The impact Q2 2022 (Apr-May) Q2 2022 (Apr-May) international trade in

regional troubles as it has Q4 2020 Q1 2021 Q2 2021 Q3 2021 Q4 2021 Q1 2022 Q4 2020 Q1 2021 Q2 2021 Q3 2021 Q4 2021 Q4 2020 Q1 2021 Q2 2021 Q3 2021 Q4 2021 Q4 2020 Q1 2021 Q2 2021 Q3 2021 Q4 2021 Q4 2020 Q1 2021 Q2 2021 Q3 2021 Q4 2021 Q12022 ELEVATED of the crisis has been felt in 2021 was largely the

resulted in a shortage of COMMODITY PRICES terms of a rise in the price of result of increases in

containers, disruptions in US Eurozone UK Japan China KEEP INFLATIONARY commodities like food, metal and US Eurozone UK Japan China (rhs) commodity prices,

shipments and logistical Source: National Sources PRESSURES AT especially energy. Oil and gas Source: Varied National Sources subsiding pandemic

difficulties in acquiring raw RECORD HIGH prices have surged over supply restrictions and a strong

materials. In many economies fears, crossing US$100 per barrel recovery in demand due

domestic recovery has been the last quarter of 2021 (Q4 monetary stimulus. However, for the first time since 2014, as CENTRAL BANKS HIKE Countries like the US and UK to economic stimulus

dampened due to elevated 2021). Throughout 2021, the slowdown towards the Inflation had already been on Russia happens to be one of the have, started increasing packages.

commodity prices (especially economic growth in the US end of the year was majorly a rise since Q2 2021, due to top producers and exporters of INTEREST RATES, interest rates and tightening

energy and food) and global has been fueled by massive due to a spike in Covid-19 persistent supply-side fossil fuels in the world. This has SIGNAL AN monetary policy in the fight

supply-chain bottlenecks fiscal stimulus as well as very cases and cautious consumer bottlenecks as demand for resulted in the fuel product AGGRESSIVE FIGHT against inflation. US in its May The latest available data

caused by limited trade low interest rates. However, spending. goods surged after reopening retailers passing the increase in TO CURB INFLATION 2022 monetary policy meet for January 2022 points

channels. plethora of factors conspired of the economies. The international oil price to the further hiked rates by 50 bps towards a somewhat

to weigh against its growth Similarly, as per the latest continuous elevation of consumers, thereby aggravating (0.5 per cent), while the UK steady growth in exports.

In tune with our expectations, during first three months of available data, the Chinese commodity prices, especially inflationary pressures. Further, Central banks across the globe hiked rates by 25 bps (0.25 However, going forward,

the IMF in its latest World 2022. US growth declined to economy expanded by 4.8 per that of energy and food Russia and Ukraine together also have, since the start of the per cent). global trade is expected

Economic Outlook has 3.4 per cent in Q1 2022, cent in Q1 2022, after driven by the Eastern account for 30 per cent of the Covid pandemic, been to moderate in the first

revised global growth largely due to the rising covid growing at an impressive rate European crisis, has wheat exports and are major maintaining an accommodative AS PER WTO, GLOBAL quarter of 2022 due to

projections downwards to 3.6 infections which in turn of 8.8 per cent in 2021. accentuated inflationary exporters of edible oils and monetary policy stance to TRADE IS EXPECTED the challenges emanating

per cent in 2022 and 2023, hampered the economic Growth in Q1 was buoyed by pressures in advanced fertilizers. Hence, the recent support growth. However, the from the ongoing

citing the Russia-Ukraine war activity, inflation surging to a monetary stimulus that economies to a 30-year high. geopolitical tensions have also ongoing conflict and the spike TO MODERATE IN 2022 Russia-Ukraine crisis as

caused the prices of wheat, corn,

which has played a significant four decades high and the supported investments and Prices of everyday essentials in oil prices has further pushed the supply chain

role in the slowdown of effects of ongoing industrial production. have also risen. cooking oil and fertilizers to rise up inflation and moderated Exports have been on a rise disruptions are unlikely

sharply resulting in high food

global growth. Further, the Russia-Ukraine crisis. However, the risk of a sharp inflation and shortages are also global growth. Therefore, there globally, with absolute to subside by H1 2022.

tightening of monetary policy slowdown in the coming Consequently, major expected to follow. is now a rethink within Central numbers registering a sharp

by major economies could Other major economies like months has escalated, amid economies, across the board, banks to wind down their recovery in Q4 2021 despite

also put a downward the Eurozone, UK and Japan widespread Covid lockdowns, have seen an uptrend in Additionally, sanctions imposed accommodative stance and supply-side constraints such as Outlook

pressure on growth in the grew at an annual rate of 5.6, a prolonged downturn in the inflation during 2021 and the by the Western countries have port backlogs and

later part of the year. 8.3 and 1.9 per cent, property sector and start of 2022, with the latest resume tightening of policy

respectively in 2021, mostly uncertainty from the war. first quarter data indicating a stunned the Russian banking and rates to contain rising prices semi-conductor shortages Overall, the key global

due to a jump in domestic sharp increase in prices financial system and are set to which could pose as a major majorly due to the economies are poised for

GLOBAL ECONOMIES consumption aided by the Going forward, the impact of across economies. exacerbate supply chain threat to the economy. restrictions imposed. a slow growth in 2022,

RECOVER IN 2021, generous dose of fiscal & ongoing Eastern-European bottlenecks. Many foreign largely because of the

HOWEVER POISED FOR This uptrend in inflation has companies, viz. Ikea, Coca-Cola, spillover impact of the

etc have exited Russia due to

A SLOWDOWN IN 2022 Headline Inflation Inching up (y-o-y%) resulted in central banks of the sanctions and political Trajectory of Exports (y-o-y%) Russia-Ukraine crisis. The

10.0 most economies to effect pressure. This has impacted 60.0 50.0 resultant elevated

8.0 8.0 tightening of monetary policy business and consumer 50.0 commodity prices and

In the past year, major 6.0 6.2 6.2 and consider hiking interest confidence is likely to suffer. For 40.0 40.0 higher input costs could

economies around the globe 4.0 rates. businesses, the impact will be felt 30.0 23.0 30.0 lead to inflationary

have managed to regain some 2.0 0.9 by way of slowdown in growth 20.0 22.7 18.1 20.0 pressures gathering

momentum and reach 0.0 1.2 0.5 1.1 However, in the case of China, and reduced profitability. 10.0 11.9 16.6 10.0 momentum. This is

somewhat close to -2.0 -0.3 -0.9 0.1 inflation rose at a 6.5 3.3 6.4 0.0 expected to nudge the

pre-pandemic levels of slower-than-expected pace, The entire global economy will 0.0 -5.7 -5.9 major central banks

economic activity. The US Q4 2020 Q1 2021 Q2 2021 Q3 2021 Q4 2021 Q1 2022 Q4 2020 Q1 2021 Q2 2021 Q3 2021 Q4 2021 Q1 2022 Q4 2020 Q1 2021 Q2 2021 Q3 2021 Q4 2021 Q1 2022 Q4 2020 Q1 2021 Q2 2021 Q3 2021 Q4 2021 Q4 2020 Q1 2021 Q2 2021 Q3 2021 Q4 2021 Q1 2022 resulting in the Chinese feel the effects of the crisis -10.0 -10.0 across the world to

economy expanded at an Q1 2022 (Jan-Feb) central bank getting ready to through slower growth, trade Q4 2020 Q1 2021 Q2 2021 Q3 2021 Q4 2021 Q4 2020 Q1 2021 Q2 2021 Q3 2021 Q4 2021 Q4 2020 Q1 2021 Q2 2021 Q3 2021 Q4 2021 Q4 2020 Q1 2021 Q2 2021 Q3 2021 Q4 2021 Q4 2020 Q1 2021 Q2 2021 Q3 2021 Q4 2021 further tighten policy

average rate of 5.8 per cent in ease monetary policy to disruptions, and steeper inflation, US Eurozone UK (rhs) Japan (rhs) China rates in the coming

2021. Its growth further US UK Eurozone Japan China cushion its slowing economy. especially harming the poorest months, to tame inflation.

accelerated to 5.5 per cent in Source: Varied National Sources and most vulnerable. Source: World Trade Organisation (WTO)

24 ANALYSIS, RESEARCH, THOUGHT LEADERSHIP & ADVOCACY ANALYSIS, RESEARCH, THOUGHT LEADERSHIP & ADVOCACY 25

QUARTERLY JOURNAL OF ECONOMICS

QUARTERLY JOURNAL OF ECONOMICS

MAY 2022 MAY 2022